Social, economic, demographic, and public policy shifts have made Gen Xer and millennial retirement security a pressing concern. In this report, we combine data from multiple sources to project how various forces might play out over the next 30 years to shape the retirement security of late Gen Xers (born in the last half of the 1970s) and early millennials (born in the first half of the 1980s).

Conflicting forces create uncertainty about Gen X and millennial retirement security

Various forces will frame the financial security of Gen Xers and millennials in old age. On one hand, their retirement security is endangered because of their decreased likelihood to get married, purchase a home by their mid-thirties, and participate in employer-sponsored retirement plans. On the other hand, they might be buoyed by their higher rates of college education and higher earnings for women.

Given these conflicting trends, there is no consensus about how Gen Xers and millennials will fare in retirement. Is a retirement crisis looming that will plunge many older adults into or near poverty, or will economic growth boost their retirement incomes?

Higher incomes, lower standards of living

We project that median incomes will be higher for Gen Xers and millennials at age 70 than for previous generations, but these generations are at a higher risk of seeing their living standards fall. When we projected incomes at age 70, we found that about 40 percent of 70-year-olds born between 1976 and 1985 would be unable to replace at least 75 percent of the inflation-adjusted average earnings they and their spouses received from ages 50 to 54. In comparison, the replacement rate will likely fall below that threshold for 32 percent of those born between 1936 and 1945 and 30 percent of those born between 1956 and 1965.

Our findings suggest that retirement security for late Gen Xers and millennials will be shaped by many of the forces that affect current retirees, including rising debt levels and the erosion of defined benefit pension plans.

Millennials are not dramatically worse off, but are not improving

Millennials are not expected to fare dramatically worse than previous generations, although the steady improvement in economic status that has defined American society since the middle of the 20th century appears to have ended, at least for now. This is especially pronounced for men, whose labor force participation rates continue to decline before age 55 and whose median wages remain stagnant.

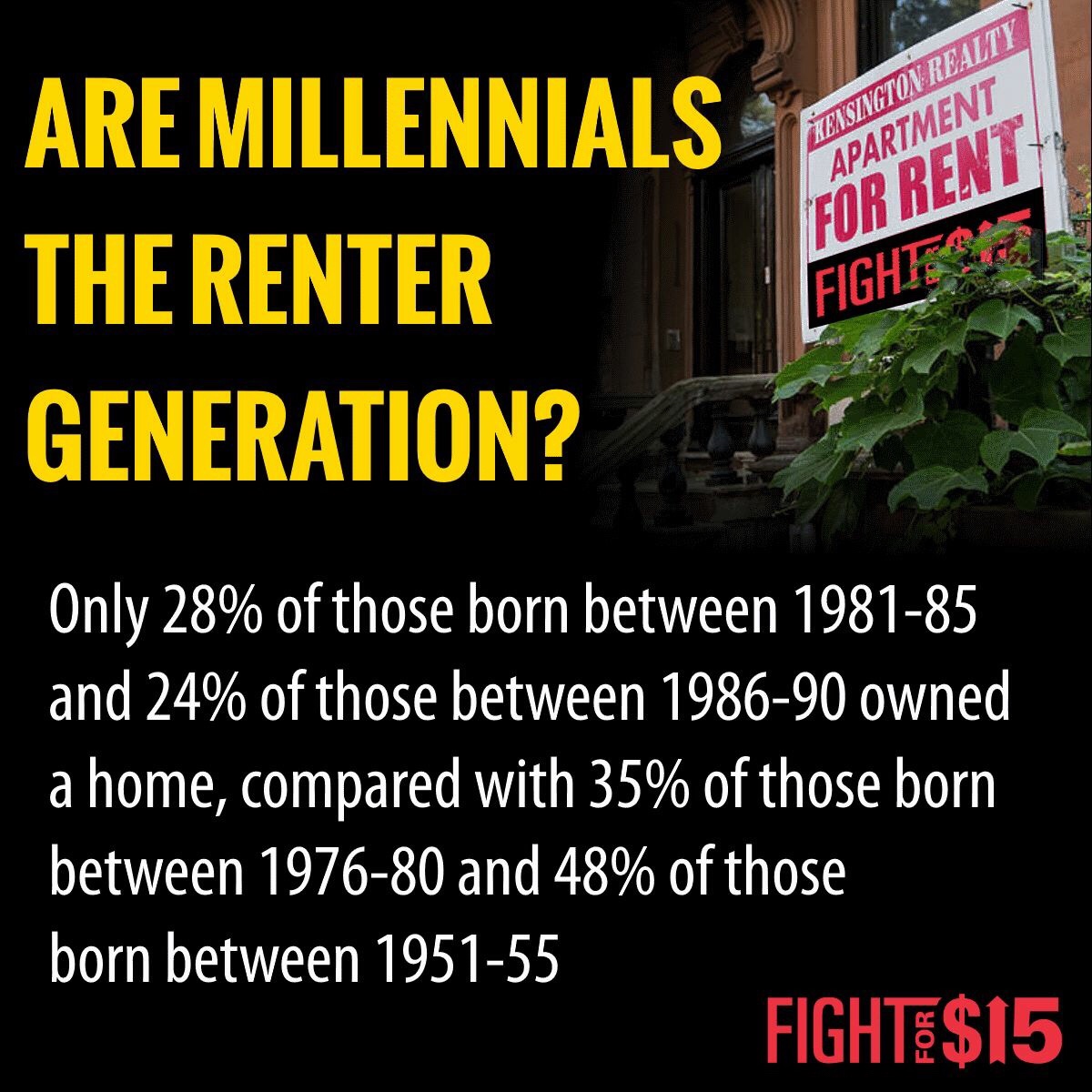

People born after 1970 are not accumulating household wealth faster than those born in the 1960s, reversing the generational growth earlier cohorts experienced. Millennials are also less likely to own a home than earlier generations.

But Gen X and millennial women are earning more than their baby boomer counterparts did, although millennials are not earning more than Gen Xers. Another promising development is millennials’ increased college graduation rates, which raises their future earnings potential.

Much is still unknown about Gen X and millennial retirement

Financial security in old age will hinge on factors that have yet to play out. The future of wage growth, stock market returns, interest rates, housing prices, and inflation will affect retirement incomes. How long people tend to work, which will depend partly on how health trajectories evolve, will help determine financial security for future retirees. Policy choices regarding retirement programs, especially Social Security, will also play a role.

Source: https://www.urban.org/research/publication/retirement-outlook-millennials

Leave a comment